- Published on

The AI wave blew up the NAND market with $46 billion in single-season revenues.

- Authors

- Name

- aimode.news

- @aimode_news

With a new wave of AI, the global NAND flash market experienced an explosion in the first quarter of 2026, with industry revenues rising 3.5 times more than in the same year, with a single-season record of about $46 billion, while the traditional PC market was under considerable pressure in high costs and demand shifts.

The latest report of the MarketPoint Research, a market research institute, shows that, as of the first quarter of 2026, global NAND market revenues had increased 3.5 times over the same period last year, with a single-season size of $46 billion, which is even higher than the total NAND income for the whole year of 2023, highlighting the current level of storage market activity under AI. The core driving force of the current round of growth is the hot tide of Agenic AI applications, the rapid expansion of large-scale data centre deployment, and the need for individual clusters to accommodate hundreds of PB-level data, which directly boosts the need for high capacity NAND storage.

Structurally, demand at the enterprise level has become the absolute mainstay of the NAND market. Statistics show that the enterprise level (mainly data centres and cloud services) accounted for about 43 per cent of the total NAND needs in the first quarter of 2026, and was considered to have surpassed 60 per cent by the end of the year, further strengthening the demand-supply and price dominance in this area. At the same time, AI continued to press the NAND contract and spot prices, resulting in a continued increase in the vendor ' s quarterly sales.

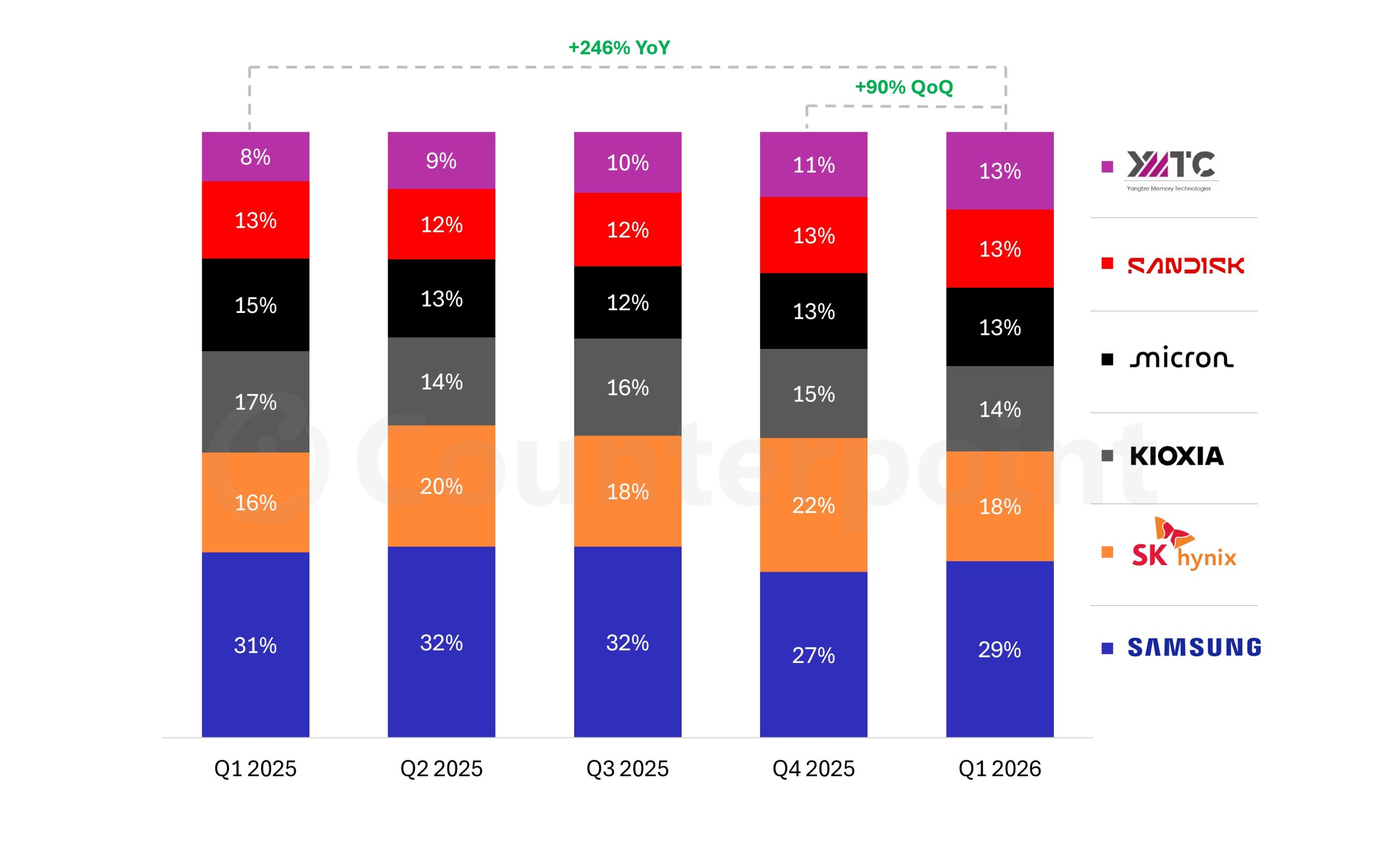

In terms of manufacturing patterns, Samsung remains at the top of the NAND market, with a market share of approximately 29 per cent, followed by SK and Kioxia, respectively, whose combined share of income has remained high. Micron and Sandisk have about 13 percent of their income, but their advantage is being strongly affected by the power of Chinese manufacturers.

Most of the attention is focused on the rapid rise of the Chinese NAND manufacturer Yangtze Store (YMTC). The latest data show that the global NAND market share of YMTC in the first quarter of 2026 has climbed to about 13 per cent, an increase of 246 per cent over the same period, significantly narrowing the gap with international producers such as Sandisk and Micron. In terms of income distribution trends, the expansion of the Yangtze storage has to a certain extent resulted in a “smuggling” of market shares from Samsung, SK Hercules and Zhang Man, reflecting a rapid increase in their capacity to produce critical technologies, such as high-level piles of NAND.

In the area of terminal storage products, Samsung remains a central force in the global SSD market. According to the report, Samsung maintained a clear lead in the global SSD market, followed by SK Hercules, while Zhang, Mei-ray and Sandisk were on the second stage. Despite the terminal PC market pressure, the overall NAND and SSD needs were not directly hampered by the macrodowns due to the continued expansion of data centres, enterprise-level storage and the AI training and reasoning platform.

It is noteworthy that the Yangtze storage is preparing to land on the capital market in China, and that the first public equity (IPO) is planned for the local stock exchange to further expand its capital capacity. Together with China's DRAM manufacturer, CXMT, the so-called “historic expansion” programme, both of which plan to construct or expand several crystal-turned plants to achieve a doubling of current production capacity, with the goal of significantly increasing domestic self-sufficiency and global voice in the storage chain in the coming years.

Unlike DRAM and NAND operations, which received AI-cycle dividends, the performance of the traditional PC market was significantly depressed. The research agency IDC predicts that global traditional PC exports will decline by about 11.3 per cent in 2026, and will remain weak in 2027, with signs of recovery expected until 2028-2029, and a real return to a healthier level of exports likely to wait until 2030. Global PC deliveries are expected to drop to about 260 million in 2026, compared to more than 290 million in the previous year.

According to industry, the pressure on the PC market comes from multiple factors. On the one hand, combined with the higher DRAM and NAND prices associated with AI-related demand, the mechanism has led to a substantial increase in the price of final sales, which has inhibited demand for consumption and traditional commercial procurement. On the other hand, a large budget has been diverted to cloud and data centre construction, and the business renewal cycle of the traditional PC has been significantly longer, making it difficult for the PC to return to high base levels during the epidemic in the short term.

Despite overall PPC market pressure, the industry is actively seeking new growth points. MacBook Neo, introduced by apples, is seen as one of the representatives of a new generation of AI PCs that uses self-study chips and integrated platforms to develop differential competitiveness in energy efficiency and performance experience. To address this trend, Intel has also facilitated the landing of new platforms, such as Wildcat Lake, some of which, like Dell XPS 13, are directly competing for MacBook Neo, trying to offer relatively close experiences at lower prices in order to compete for medium- and low-end light capital markets.

In the introductory and lower-middle-price segments, Chase is cutting into the penthouse market through the Snapdragon C series platform. The owner of the relevant product, on a “day-to-day extension” “lower full-cost” sale point, has a target range of around $300, in an attempt to provide a relative personal AI PC option in the current environment of a general increase in PC overall prices. However, from a supply chain perspective as a whole, the real cost reversal may be after the formal production of new DRAM and NAND production lines, and this time window is generally expected to be around 2029-2030, making it difficult to significantly reduce the price pressure on PC terminals in the short term.

Taken together, the new AI cycle is reshaping the income structure and industry focus of the information industry. On the one hand, high-performance computing and data centre operations, as represented by Agenic AI, continue to push up NAND and DRAM prices, leading to a single-season high income for storage manufacturers; and on the other hand, the traditional PC market, which is characterized by rising costs and shifting demand, makes it difficult to re-establish the peak of output during the epidemic in a few years. As Chinese producers accelerate their expansion, international giants add to the AI storage layout and a new generation of AI PC platforms, this pattern of erosion between the global storage and PC industries is likely to continue in the coming years.